Free 65 Oregon Form

Free 65 Oregon Form

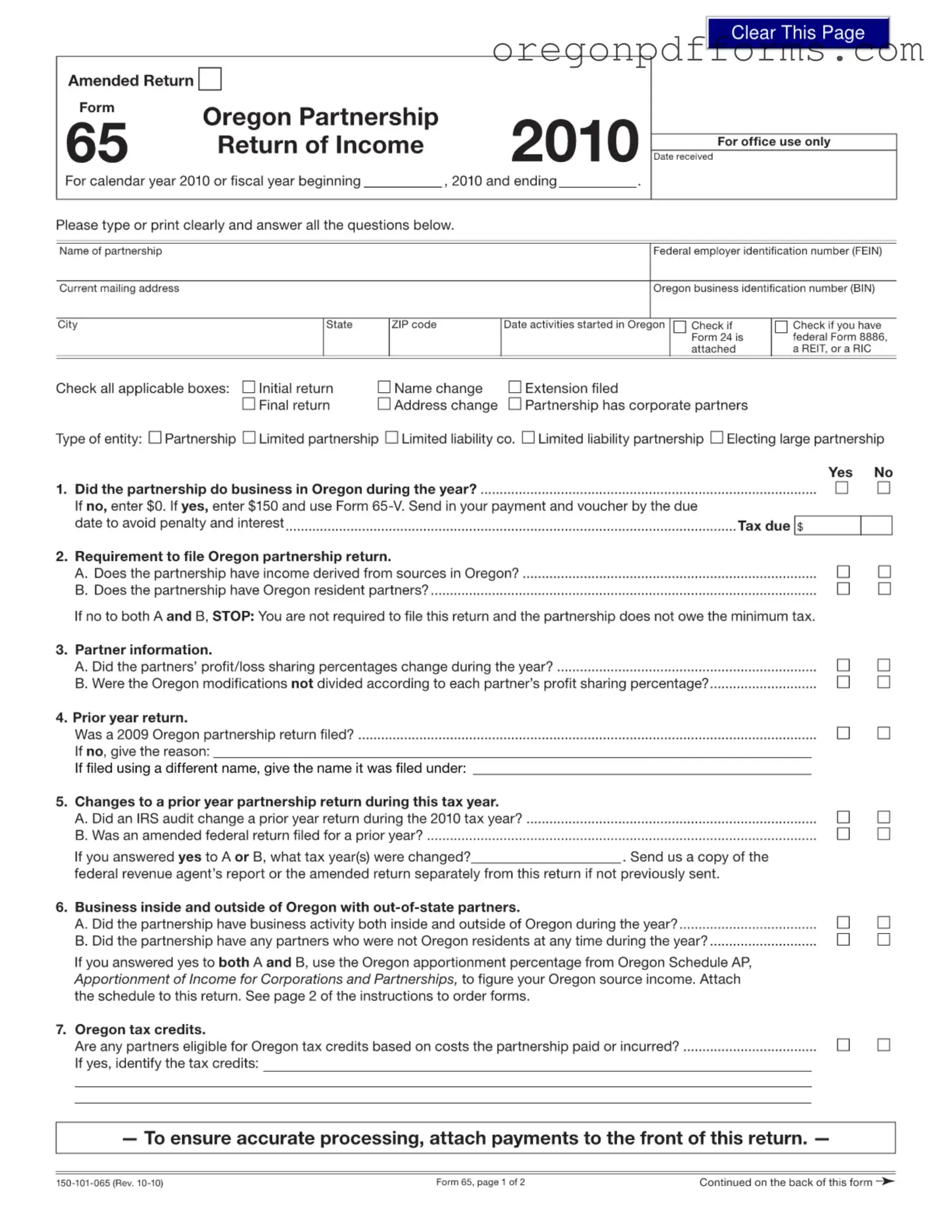

The 65 Oregon form serves as a vital document for partnerships operating within the state, encapsulating essential information regarding the partnership's income and tax obligations. Designed for partnerships that derive income from Oregon sources or have Oregon resident partners, this form not only facilitates the reporting of financial data but also ensures compliance with state tax regulations. It requires the partnership to provide critical details such as its name, mailing address, federal employer identification number, and Oregon business identification number. Additionally, the form prompts partnerships to indicate whether they are filing their initial return, a final return, or if there have been any changes in their status, such as a name or address change. One of the key components of the form is the inquiry into the partnership's business activities within Oregon, which determines the necessity of filing and the potential minimum tax due. Furthermore, the form addresses the complexities of profit and loss sharing among partners, necessitating disclosures about any changes in these percentages during the tax year. Partnerships with out-of-state partners are also prompted to report their income apportionment, thereby ensuring that all income derived from Oregon sources is accurately accounted for. The form culminates in a declaration, requiring signatures from both the taxpayer and any preparer, thereby affirming the accuracy of the information submitted. Thus, the 65 Oregon form encapsulates a comprehensive framework for partnerships to navigate their tax responsibilities while fostering transparency and accountability in their financial reporting.

Incomplete Information: Failing to provide all required information, such as the partnership name, address, and federal employer identification number (FEIN), can lead to processing delays.

Incorrect Tax Year: Not specifying the correct tax year for which the return is being filed can result in confusion and potential penalties.

Missing Signatures: The form must be signed by the appropriate parties. Omitting signatures can render the return invalid.

Ignoring Filing Requirements: Some partnerships may mistakenly believe they do not need to file if they have no income. It is essential to check if the partnership has any Oregon resident partners or income derived from Oregon sources.

Failure to Attach Necessary Documentation: Not including required schedules or forms, such as federal Form 1065, can lead to rejection of the return.

Incorrect Apportionment Calculations: Partnerships with business activities both inside and outside of Oregon must accurately calculate their Oregon source income. Errors in this calculation can affect tax liability.

Missing Tax Payments: Not submitting the minimum tax payment of $150 by the due date can result in penalties and interest charges.

Oregon Snap Periodic Report Pdf - Changes in income or expenses must be reported to maintain accurate benefits.

A Missouri Bill of Sale form serves as a legal document that records the sale and transfer of various items from one person to another within the state of Missouri. It often includes details about the item sold, the sale price, and information about the buyer and seller. Those interested in recording a sale accurately and legally are encouraged to fill out the Bill of Sale form by clicking the button below.

Money Agreement Oregon - Any disputes regarding the agreement are expected to be resolved legally or otherwise.

Oregon Tort Claim - Claimants should share any additional relevant information to support their claims.

Form 65 is the Oregon Partnership Return of Income. It is required for partnerships that have income derived from sources in Oregon or have one or more Oregon resident partners. Publicly traded partnerships taxed as corporations are exempt from filing this form. If a partnership is not required to file a federal partnership return, it does not need to file for Oregon either.

All partnerships doing business in Oregon must pay a minimum tax of $150 if they are required to file a partnership return. "Doing business" is defined as engaging in profit-seeking activities within the state. If a partnership is required to file multiple returns, the minimum tax applies to each return separately and is not apportioned.

For the 2010 calendar year, the returns and tax payments are due by April 18, 2011. If a partnership operates on a fiscal year, the return is due on the 15th day of the fourth month after the end of that tax year. It is important to note that estimated payments are not required for partnerships.

If a partnership has filed for a federal extension, it does not need to file a separate extension for Oregon. However, if an Oregon-only extension is necessary, the partnership must check the extension box on Form 65-V and submit it by the due date.

Partnerships must indicate whether there were any changes in the profit/loss sharing percentages during the year on Form 65. If there were changes, the partnership should provide details in the appropriate section of the form. This information is crucial for accurately reporting income and modifications passed through to partners.

If a partnership conducted business activities both inside and outside of Oregon during the year and had non-resident partners, it must use the Oregon apportionment percentage from Schedule AP to determine Oregon source income. This schedule must be attached to Form 65 when submitted.

| Fact Name | Fact Description |

|---|---|

| Form Purpose | The 65 Oregon form is used for the Oregon Partnership Return of Income, allowing partnerships to report their income and tax obligations in the state. |

| Minimum Tax | Partnerships doing business in Oregon must pay a minimum tax of $150 if they are required to file a return. |

| Filing Requirement | Every partnership with income from Oregon sources or at least one Oregon resident partner must file Form 65. |

| Filing Deadline | Returns for the 2010 calendar year are due by April 18, 2011, while fiscal year returns are due on the 15th day of the fourth month after the fiscal year ends. |

| Changes in Profit Sharing | Partnerships must report if the profit or loss sharing percentages among partners changed during the year. |

| Oregon Modifications | Partners must account for Oregon modifications to federal partnership income, including additions and subtractions, as specified in the form. |

| Tax Credits | Partnerships may identify Oregon tax credits for which partners are eligible based on costs incurred by the partnership. |

| Out-of-State Partners | If a partnership has business activity both inside and outside Oregon, it must use the Oregon apportionment percentage to determine Oregon source income. |

| Governing Law | The requirements for filing Form 65 are governed by Oregon state tax laws, which align with federal filing guidelines. |