Free Oregon It 1 Form

Free Oregon It 1 Form

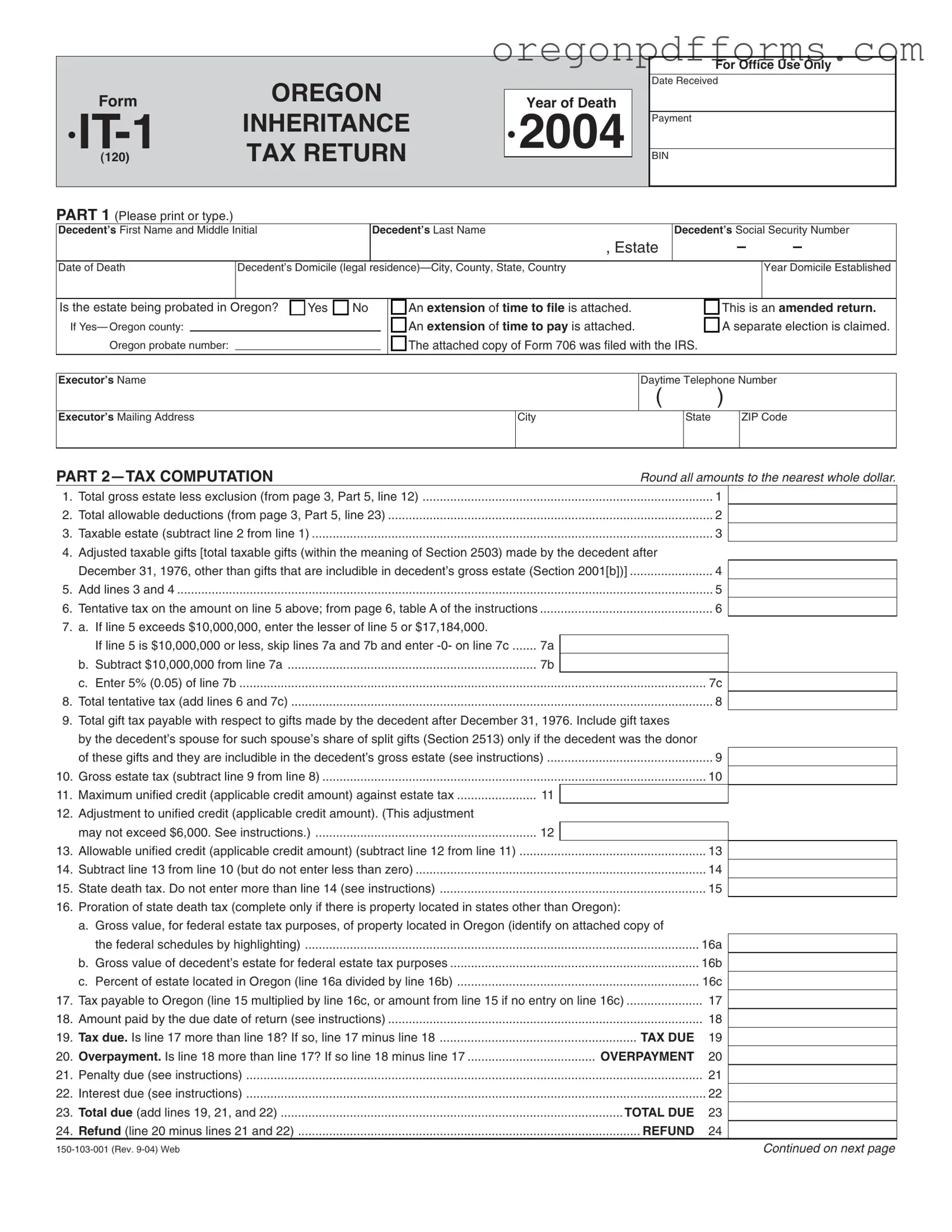

The Oregon IT-1 form is an important document for managing the inheritance tax process following a person's death. This form is primarily used to report the details of a decedent's estate, including information about their gross estate, allowable deductions, and the taxes owed. Executors must provide the decedent's personal information, such as their name, Social Security number, and date of death, as well as details about the estate's domicile and whether it is being probated in Oregon. The form includes various sections for tax computation, allowing the executor to calculate the taxable estate and any applicable credits. Additionally, it requires the executor to answer questions regarding elections related to the estate, such as alternate valuation and special use valuation. The form also mandates the attachment of necessary documents, including the death certificate, and outlines the penalties for false statements. Understanding the Oregon IT-1 form is crucial for ensuring compliance with state tax laws and for the proper administration of the estate.

Incomplete Information: Failing to provide all required details about the decedent, such as their full name, Social Security number, and date of death, can lead to delays or rejections of the form.

Incorrect Domicile Information: Providing inaccurate information regarding the decedent’s legal residence can complicate the filing process. Ensure that the city, county, state, and country are correct.

Omitting Necessary Attachments: Not including essential documents, like the death certificate or copies of federal tax returns, can result in a request for additional information, slowing down the process.

Mathematical Errors: Simple mistakes in calculations, such as rounding incorrectly or miscalculating the taxable estate, can lead to incorrect tax assessments. Double-check all figures before submission.

Neglecting to Sign: Failing to sign the form is a common oversight. Without a signature, the form is not valid and cannot be processed.

Ignoring Filing Deadlines: Missing the deadline for submitting the form can result in penalties. It's crucial to be aware of and adhere to all relevant deadlines.

Not Checking for Extensions: If an extension of time to file is needed, ensure it is properly requested and attached. Failing to do so can lead to complications.

Misunderstanding Tax Computation: Misapplying tax rates or failing to account for deductions can result in incorrect tax calculations. Review the instructions thoroughly to ensure accuracy.

Overlooking Communication Preferences: Not specifying who can receive and provide confidential tax information may delay communication with tax authorities. Clearly indicate the authorized individual(s) on the form.

State Tax Form for Oregon - Employers are advised to attach a list of work locations if there are multiple sites for minor employment.

When considering the preparation of a Power of Attorney, it is essential to utilize reliable resources to ensure the document is completed correctly. One useful resource is the Missouri PDF Forms, which can provide the necessary templates and guidance for drafting this important legal form. By taking the time to properly understand and fill out the Power of Attorney, individuals can safeguard their interests and ensure their wishes are respected in times of need.

Oregon Quarterly Mileage Tax Report - Enter the Oregon taxable miles based on public road usage in Column I.

Oregon Income Tax Forms - The required fields include your Oregon business identification number (BIN) and federal employer identification number (FEIN).

The Oregon IT 1 form is the state’s inheritance tax return. It is used to report the taxable estate of a deceased individual and calculate any taxes owed to the state of Oregon. The form must be completed by the executor or administrator of the estate and submitted to the Oregon Department of Revenue. It includes details about the decedent's estate, deductions, and the calculation of taxes due.

Any executor or administrator of an estate must file the Oregon IT 1 form if the decedent's estate exceeds the exemption threshold set by the state. Generally, estates with a gross value above a certain limit must file this return. It is essential to determine whether the estate is subject to inheritance tax, as this affects the filing requirement.

To complete the IT 1 form, the following information is typically required:

Additionally, supporting documents, such as the death certificate and copies of federal estate tax returns, may need to be attached.

The inheritance tax is calculated based on the taxable estate, which is determined by subtracting allowable deductions from the total gross estate. The form includes specific lines to report these amounts, and the tax rate is applied to the taxable estate. The instructions provided with the form detail how to use the tax tables to find the tentative tax amount, which is then adjusted based on any applicable credits.

The IT 1 form is generally due nine months after the date of death of the decedent. If additional time is needed, the executor may file for an extension. However, it is important to remember that an extension for filing does not extend the time to pay any taxes owed. Therefore, any tax due should be paid by the original deadline to avoid penalties and interest.

Yes, the IT 1 form can be amended if errors are discovered after submission. The executor must indicate that the return is an amended return and provide the corrected information. It is crucial to file the amended return as soon as possible to ensure compliance and avoid potential penalties.

If the IT 1 form is not filed when required, the estate may face penalties, including interest on unpaid taxes. Additionally, the estate could be subject to legal action by the state to collect any taxes owed. Executors have a fiduciary duty to ensure that all necessary filings are completed accurately and on time to protect the interests of the beneficiaries and comply with state law.

| Fact Name | Description |

|---|---|

| Form Purpose | The IT-1 form is used for filing the Oregon inheritance tax return. |

| Governing Law | The form is governed by Oregon Revised Statutes (ORS) Chapter 118. |

| Decedent Information | It requires details about the decedent, including name, Social Security number, and date of death. |

| Executor Details | The form must include the executor's name, contact information, and mailing address. |

| Probate Status | The form asks whether the estate is being probated in Oregon. |

| Tax Computation | It includes sections for calculating the taxable estate and any allowable deductions. |

| Filing Extensions | Extensions for filing or paying the tax can be attached if necessary. |

| Supplemental Documents | A death certificate and other necessary documents must be attached when submitting the form. |

| Election Options | The executor can make various elections, such as alternate valuation or installment payments. |

| Submission Address | The completed form should be mailed to the Oregon Department of Revenue in Salem. |