Valid Promissory Note Document for Oregon

Valid Promissory Note Document for Oregon

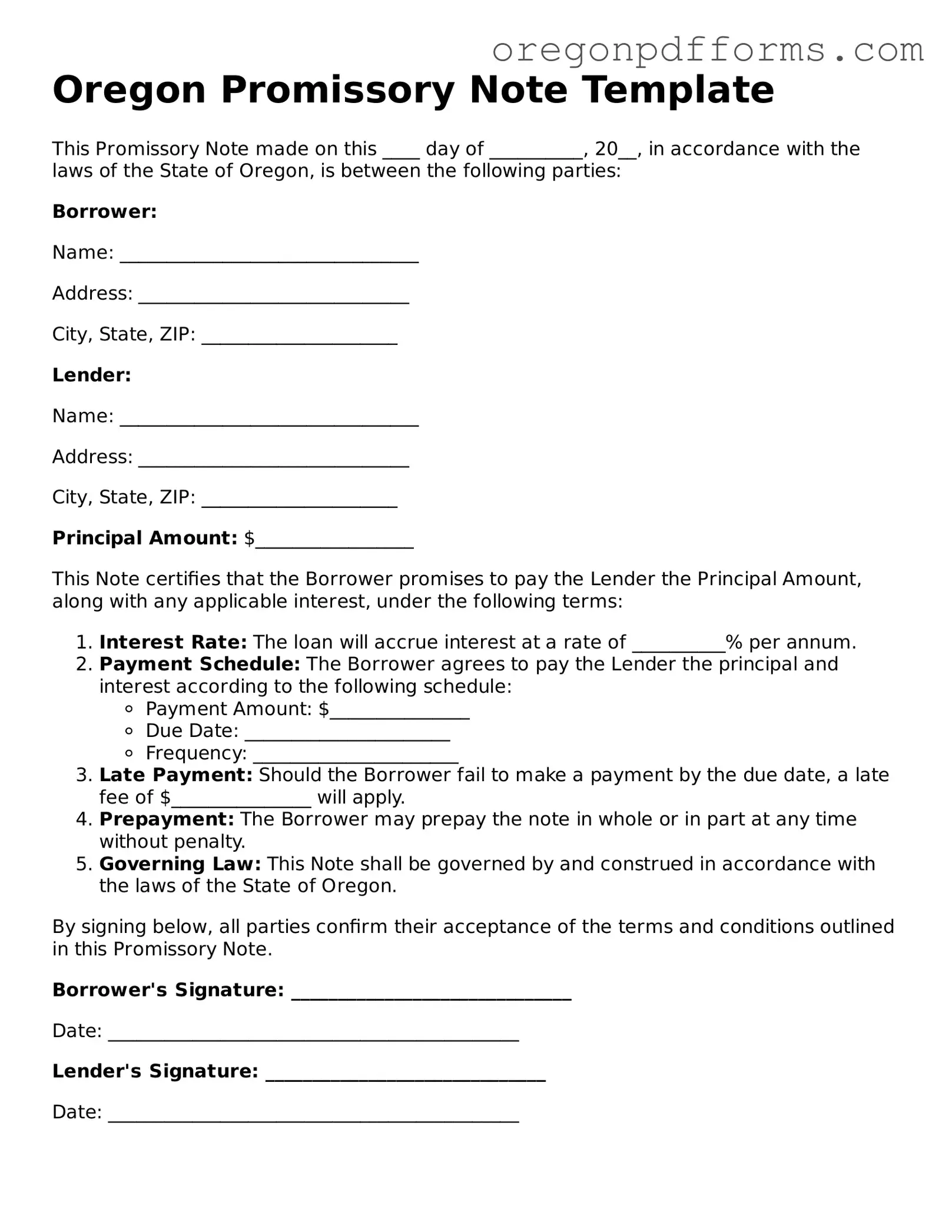

In Oregon, a promissory note serves as a crucial financial instrument that outlines the terms of a loan agreement between a borrower and a lender. This document not only establishes the amount of money being borrowed but also specifies the interest rate, repayment schedule, and any applicable fees. Essential details such as the names and addresses of both parties, as well as the date of the agreement, are included to ensure clarity and enforceability. Additionally, the form may contain provisions regarding default, allowing the lender to take specific actions if the borrower fails to meet the agreed-upon terms. By understanding the components of the Oregon Promissory Note form, individuals can better navigate their financial obligations and protect their rights in lending situations. Whether one is borrowing money for personal use or for a business venture, having a well-drafted promissory note can provide a sense of security and legal backing, making it an indispensable tool in financial transactions.

Incorrect Borrower Information: Failing to provide the full legal name of the borrower can lead to confusion. It is essential to include the borrower's complete name as it appears on official documents.

Missing Lender Details: Omitting the lender's name or contact information can complicate communication. Ensure that the lender's full name and address are clearly stated.

Improper Loan Amount: Entering an incorrect loan amount can create disputes later. Double-check the numerical figure and ensure it matches any verbal agreements.

Failure to Specify Interest Rate: Not indicating the interest rate or leaving it blank can lead to misunderstandings. Clearly state the agreed-upon interest rate to avoid confusion.

Omitting Payment Terms: Not detailing the payment schedule can result in missed payments. Specify the frequency and amount of payments to ensure clarity for both parties.

Not Including Maturity Date: Leaving out the maturity date can create uncertainty about when the loan is due. Always include this date to clarify the loan's term.

Ignoring Signatures: Failing to sign the document can render it invalid. Both the borrower and lender must sign the note to confirm their agreement.

Neglecting Witness or Notary Requirements: Some situations may require a witness or notary. Check local requirements to ensure the document is legally binding.

Not Keeping Copies: Forgetting to make copies of the signed document can lead to issues later. Always retain a copy for both parties' records.

Oregon Transfer on Death Deed Pdf - The deed can be an essential part of a comprehensive estate plan for real property owners.

Additionally, for those looking to create or manage such legal documents effectively, we recommend utilizing resources like Missouri PDF Forms, which can provide the necessary templates and guidance to ensure that all requirements are met.

Manufactured Home Title Transfer Oregon - Can be customized to fit specific needs of the transaction.

How to Complete Title When Selling Car - Must be filled out completely for validity.

A Promissory Note is a written promise to pay a specified amount of money to a designated person or entity at a defined time or on demand. In Oregon, this document serves as a legal instrument that outlines the terms of a loan, including the principal amount, interest rate, payment schedule, and any penalties for late payments. It is important for both the lender and borrower to understand their rights and obligations under the note.

An Oregon Promissory Note should include the following key elements:

While notarization is not a strict requirement for a Promissory Note in Oregon, it is highly recommended. Having the document notarized can provide an extra layer of protection for both parties. It helps verify the identities of the signers and confirms that they signed the document voluntarily. This can be particularly useful if disputes arise in the future.

If the borrower fails to make payments as agreed, they are considered to be in default. The lender has several options to address this situation:

It is advisable for lenders to document all communications and actions taken in case legal action becomes necessary.

Yes, the terms of a Promissory Note can be modified after it has been signed, but both parties must agree to the changes. This agreement should be documented in writing and signed by both the lender and borrower. It is crucial to ensure that any modifications do not violate state laws or the original terms of the note.

Yes, Oregon has a statute of limitations that applies to Promissory Notes. Generally, the time limit for enforcing a written contract, including a Promissory Note, is six years from the date of default. After this period, the lender may lose the right to take legal action to collect the debt. It is important to keep track of payment schedules and any defaults to ensure that rights are protected within this timeframe.

| Fact Name | Details |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated party at a specified time. |

| Governing Law | The Oregon Uniform Commercial Code (UCC) governs promissory notes in Oregon. |

| Parties Involved | The note involves two primary parties: the maker (borrower) and the payee (lender). |

| Interest Rate | Interest rates can be fixed or variable, and they must be clearly stated in the note. |

| Enforceability | For the note to be enforceable, it must be signed by the maker and include essential terms like the amount and repayment schedule. |

| Default Consequences | If the maker defaults, the payee may take legal action to recover the owed amount, including interest and fees. |