Free State Of Oregon Lodging Tax Form

Free State Of Oregon Lodging Tax Form

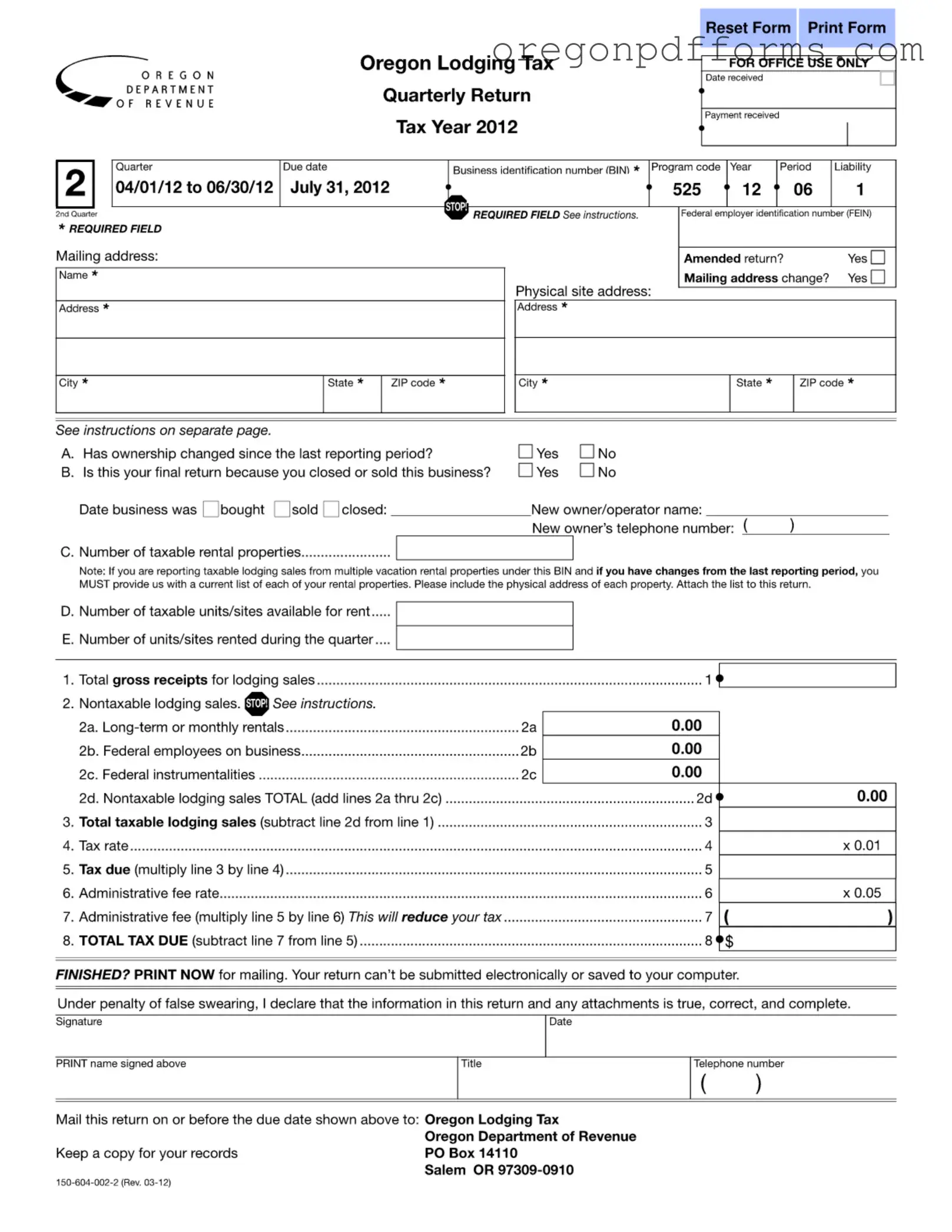

The State of Oregon Lodging Tax form is an essential document for lodging providers operating within the state. This form facilitates the reporting and payment of taxes on taxable lodging sales, ensuring compliance with state regulations. It is crucial for businesses to accurately complete the form, which includes sections for business identification, gross receipts, and nontaxable lodging sales. Providers must provide their Oregon Business Identification Number (BIN) and Federal Employer Identification Number (FEIN) as required fields. Additionally, the form asks for information about ownership changes, the number of taxable rental properties, and specific details regarding units available for rent. Understanding the distinction between taxable and nontaxable sales is vital, as it impacts the total tax due. The tax rate and administrative fees are also calculated on this form, which ultimately determines the total amount owed. Filing must occur quarterly, and it is important to note that the return cannot be submitted electronically. By adhering to these guidelines, lodging providers can maintain compliance while contributing to the state’s revenue through the lodging tax.

Incorrect Business Identification Number (BIN): One of the most common mistakes is entering the wrong BIN. This number is essential for processing your return. Always double-check it to ensure accuracy.

Neglecting Required Fields: Failing to fill out all required fields, such as the Federal Employer Identification Number (FEIN) and mailing address, can lead to your return being rejected. Make sure to complete all mandatory sections.

Not Reporting All Rental Properties: If you have multiple rental properties, you must report each one under your BIN. Forgetting to include a property can result in penalties. Always attach a current list of all properties if there have been changes.

Miscalculating Taxable Units: Accurately counting the number of taxable units available and rented is crucial. Errors in these calculations can affect your total tax due. Take your time to ensure these numbers are correct.

Omitting Nontaxable Sales: If you have nontaxable lodging sales, you must fill out the relevant lines. Failing to do so can lead to an inaccurate tax calculation. Be diligent about identifying and reporting these sales.

Not Filing a Zero Return: If no tax was collected during the reporting period, you still need to file a return indicating zero tax due. Ignoring this requirement can lead to complications.

Using Red Ink: It may seem trivial, but using red ink on your return can cause issues. Stick to black or blue ink to ensure your form is processed correctly.

Failing to Sign and Date the Return: Always remember to sign and date your return before mailing it. A missing signature can delay processing and lead to additional penalties.

Oro Step Application - Indicate your city, state, and zip code for both your physical and mailing addresses to maintain accurate records.

The Form I-864A, Affidavit of Support Under Section 213A of the INA, plays a vital role in the immigration process, as it solidifies the commitment between a sponsor and a household member to provide financial backing for an intending immigrant. By completing the form, both parties ensure that the immigrant has the financial support necessary to avoid becoming a public charge. For those looking to understand the nuances of this important document, the I 864A Affidavit Of Support form provides valuable information and guidance.

Oregon Income Tax Forms - The form must include a complete copy of your federal Form 1120S and all associated schedules.

Oregon Teacher License - Before submitting, careful review of the application is highly recommended.

The Oregon Lodging Tax is a tax imposed on each overnight stay in a temporary dwelling unit used for human occupancy. This tax applies to various lodging providers, including hotels, motels, and vacation rentals. It is collected quarterly and must be reported and paid by all eligible lodging providers.

All lodging providers in Oregon who collect lodging fees are required to file the Oregon Lodging Tax form. This includes hotels, motels, vacation rentals, and other temporary dwelling units. If you have any taxable rental properties, you must register and file a tax return quarterly, even if no tax was collected during that period.

To complete the form, follow these steps:

If your business has closed or changed ownership since the last reporting period, you must indicate this on the form. You will need to check "Yes" for the final return and provide the date of closure or sale, along with the new owner's name and contact information. A final return must be filed immediately, and any tax due must be paid.

Nontaxable lodging sales include specific categories that are exempt from the lodging tax. These include:

When completing the form, ensure you accurately report any nontaxable sales to avoid discrepancies.

The Oregon Lodging Tax form must be submitted by mail. It cannot be submitted electronically. After completing the form, print it, sign it, and send it along with your payment (check or money order) to the Oregon Department of Revenue at the specified address. Keep a copy of the form for your records.

| Fact Name | Details |

|---|---|

| Governing Law | The Oregon Lodging Tax is governed by Oregon Revised Statutes (ORS) Chapter 320. |

| Filing Frequency | Tax returns must be filed quarterly by all eligible lodging providers. |

| Due Dates | Returns are due on the last day of the month following the end of each quarter. |

| Required Information | Business identification number (BIN) and federal employer identification number (FEIN) are mandatory fields. |

| Amended Returns | If changes are needed, check "Yes" for amended returns and provide updated information. |

| Nontaxable Sales | Specific categories of nontaxable sales include long-term rentals and federal employees on business. |

| Tax Calculation | The total tax due is calculated by multiplying taxable lodging sales by the applicable tax rate. |

| Submission Method | Returns must be printed and mailed; electronic submission is not allowed. |